Tech bounce continues as focus turns to US data

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US envoys in Doha to meet mediators but not Iranians, Qatar says

* Lower oil prices ease pressures on ECB to act, says official

* Eurozone June inflation likely slowed as oil prices eased lower

* Gold endured worst quarter in more than a decade as retail frenzy fades

FX: USD was very marginally higher at the close just above 101. It was a relatively quiet day with key US data releases ahead including ISM manufacturing and NFP on Thursday. White House advisor Hassett’s comment yesterday suggesting Thursday’s NFP data could be “another strong jobs report” may have helped buck sentiment, although he also commented that arguments for a rate hike were “not so strong”. US job openings were broadly unchanged, remaining above expectations, while Consumer Confidence disappointed.

EUR climbed above 1.14 but gains are needed through 1.15 to see a pick up in bullish momentum. ECB President Lagarde said the Iran war had generated “significant” inflationary pressure and that it was not correct to describe the June move as an “insurance” hike, implying more tightening could come. Regional state inflation data reflected decelerating inflation over the June year, pointing to downside risks to the preliminary June national CPI data.

GBP moved modestly into the green having recovered its small losses through the day. The recent new 2026 low was just above 1.3150. Final UK GDP Q1 data showed no change (+0.6%) q/q but a small downward revision y/y. Domestic politics saw PM Starmer announce the long awaited defence spending plans, which are meant to survive the change at #10. EUR/GBP is hovering on strong support above 0.86.

JPY underperformed as the major powered through the 162 supposed ‘line in the sand’ regarding intervention to multi-decade highs/lows for the yen. There was jawboning from a few officials including talk that action could comprise decisive action as agreed in the joint statement with the US.

US stocks: The S&P 500 added 0.78% to close at 7,499, the Nasdaq closed up 1.69% at 30,276 and the Dow Jones settled higher by 0.26% at 52,318. Tech led the gainers by some distance (+2.55%) with only three other sectors in the green. Defensives lagged including Real Estate, Utilities, Consumer Staples and Healthcare the big underperformers. The equal weighted S&P 500 closed flat with no major driver behind the moves. The Dow Jones gained more than 12% in the first quarter, its best one since the final three months of 2022. Quarter-end rebalancing may have provided some support to indices. Chipmakers extended their rebound encouraged by strong guidance from semi producers. Nvidia moved 2.6% higher, Marvell jumped 7.3% and Intel advanced 6%.

Asian Stocks: Futures are mixed. APAC stocks traded mixed into quarter end, even as the Dow and Nasdaq performed well. The ASX 200 traded little changed and after hawkish but not unexpected RBA minutes. The Nikkei 225 rallied but swung into both red and green amid a weaker yen and intervention risks. Hang Seng and Shanghai Comp lagged as losses in miners and energy offset a tech rebound.

Gold slid towards a new cycle low at $3,942, beating the recent bottom at $3,959. But prices rebounded and printed a doji candle denoting indecision.

Day Ahead – Eurozone inflation, Sintra, US ISM Manufacturing

Consensus sees the headline ticking down two-tenths to 3.0% due to lower energy prices, and core is forecast to remain steady at 3.0%. Falling transport fuel prices are expected to more than offset the increase in household utility bills. Favourable base effects are seen helping the core ease. Importantly for the ECB, services inflation is predicted to rise modestly to 3.6%. Recent ECBspeak has underlined that despite the fall in oil prices, there is still a risk of second-round inflation effects and sticky services inflation.

The ECB Forum on Central Banking, held in Sintra in Portugal, is an annual ECB event that brings together central bank governors, academics, financial market representatives and journalists. There will be a policy panel on Wednesday afternoon European time including Fed Chair Kevin Warsh, BoE Governor Andrew Bailey, ECB President Christine Lagarde and Bank of Canada Governor Tiff Macklem. It is also worth watching out for media interviews of policymakers.

June ISM manufacturing activity is expected to print at 53.9 from 54.0, while prices paid are predicted to ease to 77.5 from 82.1. The report may be modestly softer but will still be supportive of growth in the industrial sector. As a proxy, S&P Global’s June flash manufacturing PMI rose to 55.7 from 55.1, a 49-month high, while the manufacturing output index rose to the strongest in 59 months at 57.7.

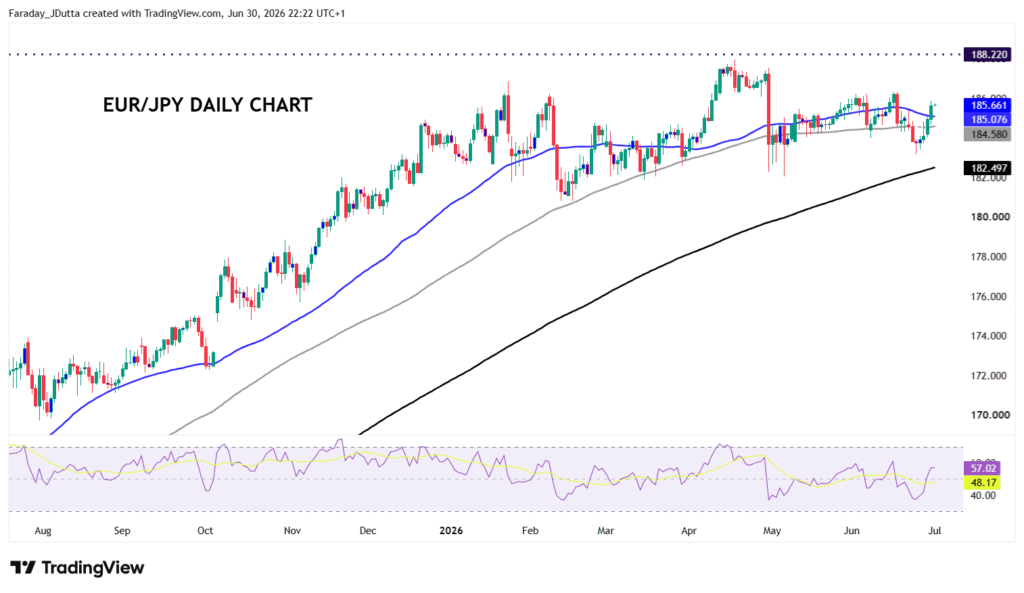

Chart of the Day – EUR/JPY awaiting catalyst

All eyes are on the Ministry of Finance in Tokyo as they contemplate if and when they will intervene in currency markets and USD/JPY. Having sold just over $70bn in late April/early May at levels just above 160, the authorities are widely expected to take action again over the coming days and weeks. Any intervention will impact other yen pairs, but Tokyo will appreciate that intervention can only try to slow, not reverse, the current major bull trend. A reversal would require not only BoJ rate hikes, but also a turn in the broad dollar trend which will need current Fed hawkishness to fade. On the euro side given recent energy dynamics, September is now seen as more likely than July for another ECB hike. Money markets assign a 32% chance of a hike in July and a 70% chance of a move in September. As for this pair, sideways range trading around 184.50 has been going for most of 2026 with highs not able to break the long-term top from 1990 (!) at 188.22. Support sits at the 200-day SMA 182.49.