Dip buying sees Big Tech bounce; yen posts 40-year low

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Trump says Iran has requested a meeting with US, Iranian officials deny

* Iran rejects Macron-backed Strait of Hormuz demining plan

* Dollar slips from 14-month high, JPY reaches 40-year low

* US stocks climb led by tech, SpaceX jumps on rapid entry to Nasdaq 100

FX: USD was lower for a third straight day as the rally over the past two weeks stalled. Fed rate risks have faded with less than an 80% chance of a hike by September as Treasury yields have followed falling crude oil prices more recently. The peace MOU between the US and Iran is fragile but holding after the weekend skirmish. Any repricing of this risk would boost the greenback as a clear bullish driver. The monthly NFP report is released on Thursday due to the US holiday, with JOLTS, ADP and ISM manufacturing ahead. New Fed Chair Warsh appears at the ECB Sintra conference on Wednesday and Friday.

EUR moved off its recent lows to the prior 2026 bottom just above 1.14. Much focus is on the ECB’s Sintra forum with President Lagarde largely validating market pricing for another hike this year, but with dovish vibes. June CPI data on Wednesday is forecast to signal a stalling trend, though prices still remain elevated. This should keep a mildly hawkish bias from speakers in Portugal, in order to keep inflation expectations in check.

GBP outperformed as soon-to-be PM Burnham outlined his plans as leader. Crucially for markets, he said he would stick to the fiscal rules, even as a noted left-wing candidate for Chancellor, Ed Milliband, became the new favourite to take over at number 11. Burnham is poised to take over at number 10 on July 20. Cable is consolidating above the recent new 2026 low just above 1.3150.

JPY underperformed as haven demand ebbed and the major edged higher into 162 and a 40-year high. Markets are watching to see if intervention could take place later in the week, either on a soft NFP or even on Friday when liquidity will be thin due to the US holiday period. Separately, a report was released around concern that the government could try to dissuade the BoJ from hiking rates to curb inflation.

US stocks: The S&P 500 added 1.17% to close at 7,440, the Nasdaq closed up 2.25% at 29,775 and the Dow Jones settled higher by 0.59% at 52,188. Seven sectors were higher with Communication Services and Consumer Discretionary rising 3.11% and 2.68% respectively. Comcast soared the most in nearly two decades on news it plans to split NBC Universal and Sky into a separate publicly traded company, boosting Comms Services. Materials was the big underperformer. SpaceX jumped 7% as it is set to join the Nasdaq 100 next week. That means forced buying by ETFs which track the tech-heavy index. Apple continued to underperform its Mag 7 peers after the 5% drop last week due to 20% price hikes on new MacBooks and iPads. Tesla surged 8.5% on upwards delivery revisions by Wall Street analysts, while Elon Musk said the EV maker had begun rolling out a new version of its FSD software.

Asian Stocks: Futures are mixed. APAC stocks traded mixed as geopolitical tensions rose between the US and Iran after tit-for-tat strikes. The ASX 200 was rangebound with tech and telecoms strength offset by weakness in utilities and industrials. The Nikkei 225 eased back below 69,000 on tech selling. The Hang Seng and Shanghai Comp were positive as Hong Kong outperformed on biotech strength.

Gold slid back towards $4,000asgeopolitical tensions moderated somewhat meaning bullion lost some of its haven allure. The recent cycle low sits at $3,959.

Day Ahead – RBA Minutes, JOLTS job data

After three straight rate hikes, the RBA left the cash rate unchanged at 4.35% as expected at the most recent meeting. The language remained hawkish citing persistent inflation and oil supply disruptions, as it warned of potential further hikes if necessary. Policymakers said short-term inflation expectations sit above levels seen earlier in 2026, with headline and underlying inflation remaining too high. Evidently, the Board is focused on its mandate to deliver price stability and full employment, though energy prices have been falling since the meeting, so the minutes may appear a little stale.

Markets will closely monitor JOLTS figures as a first steer on hiring, quits and layoffs, ahead of Thursday’s NFP report. Elevated job openings and excessive wage pressures can lead to higher inflation, prompting the Fed to raise rates, or at least keep them higher for longer. On the flip side, cooling job data can encourage money markets to reduce bets any policy tightening. Consensus forecasts 7,300k job openings, down from the prior 7,618k, which was one of the strongest readings in nearly two years. Goldman Sachs estimates a 7,100k print from online measures of job postings from Indeed and LinkUp.

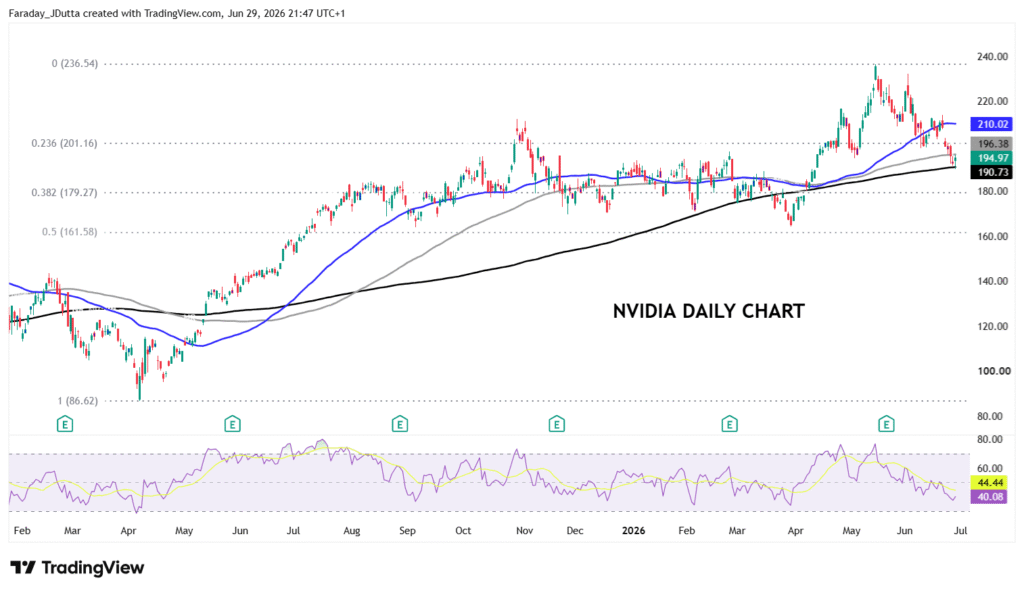

Chart of the Day – NVDA bounces off 200-day SMA

The world’s biggest company by market cap recently dipped below the historic $5 trillion mark. Nvidia has also underperformed the broad-based benchmark index this year, with the giant chipmaker rising just over 4.5%, versus an 8.7% gain for the S&P 500. Tech has suffered recently as investors have rotated into more quality and defensives after underperformance and as earnings growth advantage narrows. Chartwise, prices touched the 200-day SMA on Friday, now at $190.73 and are just below the 100-day SMA at $196.38. The major Fib retracement level (38.2%) of the April 2025 to May 2026 move sits at $179.27, with the minor (23.6%) at $201.16.