Hawkish Warsh Fed lifts USD, downs stocks & gold

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

- Clear hawkish Fed shift sees FOMC split down the middle

- US yields jump as Fed dot plot boosts bets on 2026 rate hike

- USD storms higher, euro folds as Fed trades cuts for hikes

- Stocks fall, Space X down for first time since blockbuster deal

Forex

USD was mildly bid into the Warsh’s first FOMC meeting as policymakers left rates unchanged. But the hawkish Fed statement and dot plots, which saw nine officials see at least one hike by December, pushed the greenback to 10-week highs. The median projection now implies one 25bp rate hike versus one rate cut in the prior March projections. Inflation forecasts were revised higher, unemployment and growth slightly lower which feels stagflationary. But there was a heavy inflation tilt and no dovish tone to the first Warsh press conference. He also said that by the end of the year, he would not be surprised if there is a new communications framework and changes to the dot plots.

EUR fell sharply on the Fed meeting after initially looking like it might print an inside day as prices tracked around 1.16. The three major long-term SMAs (50,100 and 200-day) have congregated above at 1.1670/75. Prices dropped to early April lows. Comments from ECB policymakers have generally remained hawkish, leaning toward at least one more 25bp rate hike. Money markets are still pricing in at least one additional hike, implying about 20bps of tightening for September and nearly one full hike by October.

GBP dipped and underperformed as CPI missed on the core and headline, though services inflation was marginally hotter. BoE rate hike expectations moved lower with UK-US rate differentials hitting fresh lows, to levels last seen around one year ago. Ahead of the BoE meeting, the latest jobs data gets released. The jobless rate should remain at 5% and wage growth is forecast to cool to 2.9%.

JPY topped its peers, but it was still another relatively quiet range day. Yield spreads are showing tentative signs of stabilisation and a softening in the Fed’s outlook would be expected to deliver material JPY strength and a recovery from current levels. The longer-term bull trend in USDJPY is showing signs of exhaustion, with meaningful resistance above the 160 level and additional anticipated resistance closer to 162.

Stocks

US stocks: The S&P 500 lost 1.21% to close at 7,420, the Nasdaq closed down 0.99% at 29,671 and the Dow Jones settled lower by 0.97% at 51,498. Communication Services, Consumer Discretionary and Real Estate led the laggards, with all sectors in the red and Industrials just modestly lower (-0.12%).Post the Fed meeting, money markets gave a 90% chance of a 25bp rate hike by December. Microsoft led the Mag 7 lower, down 5.4%, as it walked away from a $3bn deal to lease Oracle cloud capacity over security concerns. Intel jumped 3.5% as it said its new chip process has entered risk production. SpaceX fell 5% after a three-day surge had pushed its market cap above Amazon to the fifth biggest firm on the globe.

Asian Stocks: Futures are mixed. APAC stocks traded mixed after the muted Wall street handover. The ASX 200 eventually turned higher led by mining, and tech though this was offset by energy and defensives lagging. The Nikkei 225 printed a record top briefly topping the 70,000 mark. The Hang Seng and Shanghai Comp lagged amid losses in autos and aluminium producers.

Gold

Gold fell for the first day in four, its best run since late March. The hawkish Fed meeting pushed up the odds of a Fed rate hike. The 200-day SMA sits at $4,436.

Day Ahead – Bank of England Meeting

The MPC will leave rates unchanged at 3.75%, with a widely watched vote split expected at 8-1. Recent data has been mixed, with May PMIs suggesting the economy came to a marked slowdown following a solid April print, as the service sector index took its steepest decline in four years. Q1 GDP was high at 0.6% but retail sales reflected the deteriorating consumer sentiment in April with the biggest monthly decline in a year. Yesterday’s CPI numbers were softer than forecast with wages also easing.

Rates are currently seen as somewhat restrictive so that gives the bank space to assess how conditions develop. Forward guidance will be key, with Governor Bailey describing the prior meeting decision as an ‘active hold’. But he has been mostly dovish leaning, arguing that allowing inflation to run above target is justified given the uncertainty about the impact of the Iran war on the economy and the weak pace of growth. We could quickly be back in a situation with a completely split MPC which potentially means the BoE sit on their hands for some time.

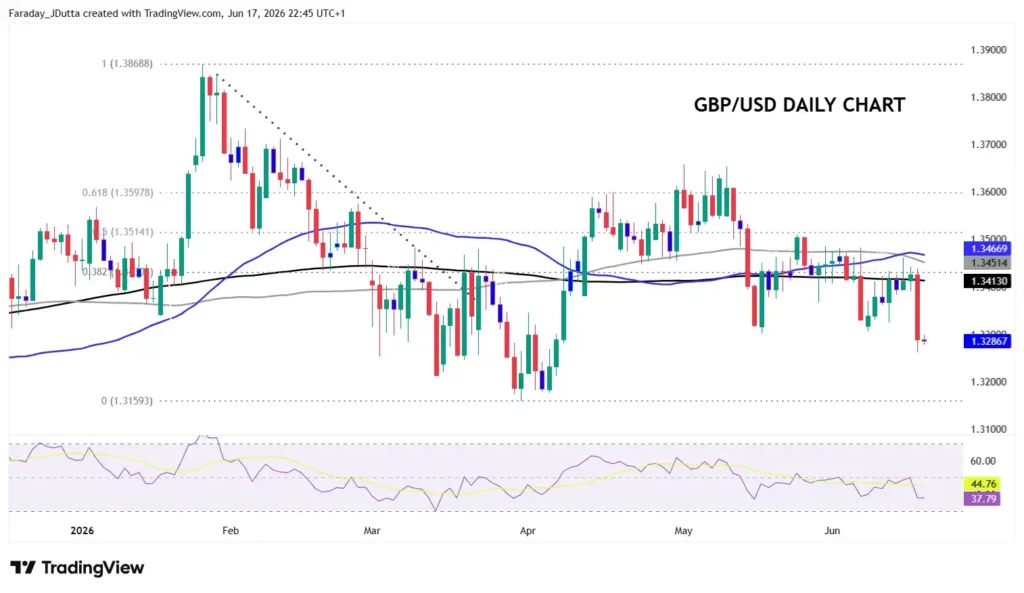

Chart of the Day – GBP/USD messy

The US-Iran deal has seen rate hike expectations fall with markets now pricing in around a 25% chance of a July rate rise and just one increase this year, down from a peak of above three. If inflation has peaked, then rate cuts could be in play instead by next year, in a similar scenario to before the conflict. Cable has been messy recently after trading around a major Fib level of this year’s high and low at 1.3430. Prices turned sharply lower yesterday as the 200-day SMA acted as resistance again at 1.3413. The major has struggled above here over the past few sessions. Recent lows sit just above 1.33 and then just below 1.32, while the 50-day SMA is at 1.3466 and late May highs at 1.3509.