Crude hit, stocks mixed, GBP bid and JPY on intervention watch

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US Treasury department authorises Iranian oil sales through August

* US Vice President JD Vance hails ‘great progress’ in US-Iran talks

* UK’s PM Starmer resigns, Burnham says too soon for election talk

* SpaceX down 16.4% as it turns to the bond market for infrastructure spending

FX: USD consolidated before finding a bid, after it posted a 13-month high at 101.12 last week, above the year-to-date March peak at 100.64. Oil prices whipsawed but US-Iran talks were said to be positive and constructive. The hangover from last Wednesday’s hawkish Fed and first Warsh meeting lingered. The question for us is whether inflation has now peaked and this is ‘peak Warsh’? There’s a one in three chance of a July 25bps hike, that was 6% one week ago. Thursday’s core PCE figures are from May so before the recent sharp fall in oil prices. We may have to wait a few months to get a proper read on fresh data.

EUR underperformed as the world’s most popular currency pair printed an inside day and consolidated near recent lows. ECB comments have generally leaned neutral/hawkish, with policymakers squarely focused on the risks of second-round inflationary pressures. ECB rate expectations have been relatively steady over the past month or so, pricing in about 22bps of tightening for September. That said, Lagarde said she sees no need for a more forceful ECB response to the Iran war.

GBP was the major outperformer on the day that PM Starmer resigned. It was classic sterling price action with fiscal worries over likely new PM Burnham overblown, as gilt yields actually slid on the day. See below for more.

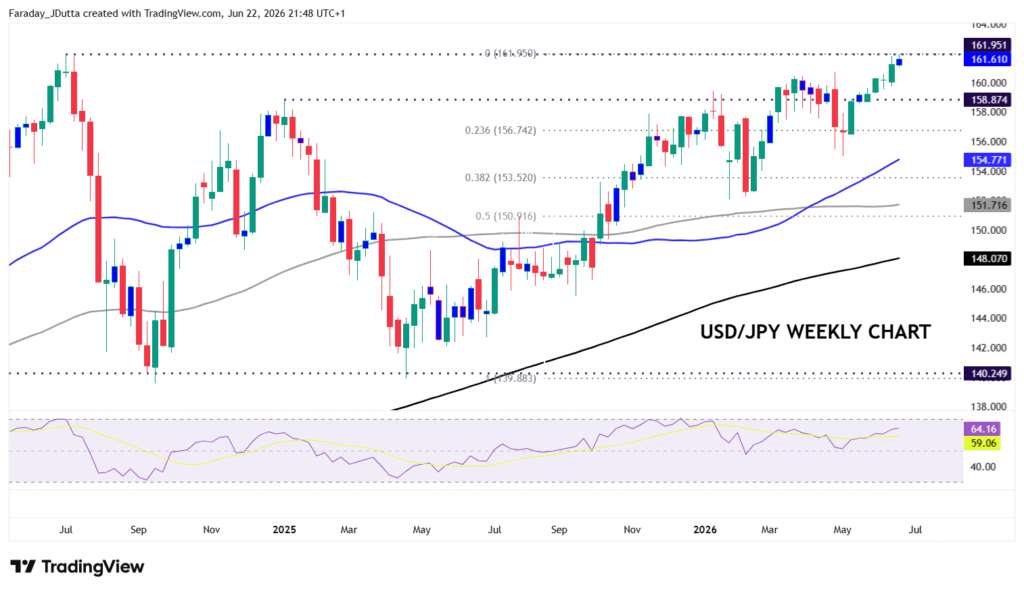

JPY was mid-pack as the major made fresh cycle highs at 161.92 before paring gains. Markets were on high alert for intervention activity and price action, with the long-term top from July 2024 at 161.95.

US stocks: The S&P 500 lost 0.34% to close at 7,475, the Nasdaq closed down 0.19% at 30,347 and the Dow Jones settled lower by 0.29% at 51,713. Sector performance was mixed, with Real Estate, Energy and Health Care outperforming, while Communication Services and Consumer Discretionary were the clear laggards. A key driver of the weakness in the Nasdaq and the S&P 500 was pressure on Alphabet (-5.1%), after DeepMind Vice President John Jumper departed the company to join Anthropic. Micron jumped 6.8% as it announced a strategic agreement also with Anthropic to scale next-generation AI infrastructure. The SOX semiconductor index hit fresh highs. SpaceX plunged over 16% as the Elon Musk space company turned to the bond market as it shifts its AI infrastructure spending into hyperdrive.

Asian Stocks: Futures are mixed. APAC stocks traded mixed with choppy price action on conflicting Middel East headlines. The ASX 200 struggled for direction on gold and financials strength competing with tech and energy weakness. The Nikkei 225 rallied more above 72,000 to fresh record highs on tech strength and softer oil and the yen. The Hang Seng and Shanghai Comp were mixed with rising trade tensions evident after China added 10 US firms to its export control list.

Gold fell for a third straight day as the hawkish Fed and higher rates made the non-yielding asset less attractive. Goldman Sachs expects central bank gold buying to slow slightly but remain a structural floor for prices in the next couple of years.

Day Ahead – PMIs, UK PM

PMIs are forward-looking indicators that should provide a sense not just of overall activity but also of the ongoing “dispersion” theme. That is, the resilience of the US economy against the sluggishness threatening Europe and potentially reinforcing last week’s household numbers (including retail sales). More broadly, business confidence is expected to recover after the signing of the US-Iran agreement, but it could be too early to gauge the full impact. Worryingly high price pressures are predicted to cool and change the outlook going forward. Sluggish growth in services will be in focus.

Sterling was the sole G10 currency in the green against the greenback on Monday, and saw little move after PM Starmer resigned, leading the way for Burnham to lead his PM campaign. UK assets were bid after possible challenger Streeting released a statement endorsing Burnham and significantly reducing the odds of a leadership contest. That appears to set Streeting up to be Chancellor, an outcome which would be much more welcome than other options, such as the more left wing Energy Secretary Miliband. The next Chancellor is the key position for markets. Betting markets see a 78% chance of Streeting being the next occupant of #11 Downing Street (where the Chancellor lives!) Incumbent Chancellor Rachel Reeves has successfully mitigated market concerns via a strong commitment to the fiscal rule. Markets will search for similar reassurances from her successor.

Chart of the Day – USD/JPY close to key long-term level

We talked about the new market moniker – ‘Trade the data, not the Fed’ last week and in our weekly commentary. New Fed boss Warsh is unimpressed with forward guidance, dot plots and any previous Fed forecasts, also reminding us that the FOMC hadn’t hit their inflation target in five years. The new very short statement could also be summed up with its final sentence – “The Committee will deliver price stability.” That means it’s a tough battle for the Japanese authorities when the Fed is deemed this hawkish and yields spreads are very much against you. We note reports in the Nikkei that the Japanese Finance Minister Katayama and US Treasury Secretary Bessent held talks online, where they likely discussed the foreign exchange market. The July 2024 top is key at 161.95, with the April 2026 high at 160.72. A soft US core PCE figure would help the MoF with US gas prices already coming down.