Tech stocks bounce ahead of Samsung numbers, USD quiet

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Trump: US prefers Iran nuclear deal, military action remains an option

* Fed’s Waller says ‘forward guidance’ needs to be flexible

* Broadcom, Apple extend chip supply deal through 2031

* Yen weakens again, reverses last week’s late strength, back above 162

FX: USD kicked off a quiet risk event week with a small bid for most of the day before closing flat, after the recent sell-off post-Thursday’s monthly jobs report. Essentially, that data gives the FOMC more time to assess incoming economic figures and takes the pressure off rate setters to go through with more policy tightening. There’s around 30bps of rate hikes priced in for 2026, from a peak above 43bps. The next key data point is next week’s CPI, which new Fed Chair has said is the bank’s major focus. The prior 2026 top from late March sits at 100.64. ISM Services very mildly missed estimates while prices paid eased to the lowest since February and employment returned to expansion for the first time in four months.

EUR was virtually unchanged on the day with a quiet trading range. A September rate hike from the ECB is now priced with less than coin flip chance, but it is too early for the ECB to sound the ‘all-clear’ on inflation. That is due to the risk that core inflation could still edge higher over the coming months. ECB speakers this week, including heavy hitters such as Isabel Schnabel and Philip Lane, are likely to want to keep that message front and centre.

GBP outperformed its peers on little major news. Markets are pricing little change for either of the next two (July 30, September 17) Bank of England meetings, with 50:50 chance more or less of tightening for November and 17bps by December. UK political news is brewing with Andy Burnham likely to become the next PM on 20 July, with the new Chancellor announced shortly after. The favourite is the more left leaning Ed Miliband, though markets remain relatively calm. The problem remains, however, that there is very little fiscal room for adjustment without raising taxes.

JPY was the big underperformeras prices in the major reversed nearly all the selling from last Thursday and closed just above 162 again. That sell-off was rumoured to be intervention but we won’t know officially for some time. The MoF in Tokyo didn’t show up in holiday-thinned conditions on Friday. This could be a reminder that officials want to use their finite FX reserves cautiously. The next window for intervention could mid-July ahead of the next public holiday in Japan.

US stocks: The S&P 500 added 0.72% to close at 7,537, the Nasdaq closed up 1.26% at 29,698 and the Dow Jones settled higher by 0.29% at 53,061. Stocks closed higher following the long Independence Day weekend, with the Nasdaq outperforming as Technology led the advance. Semiconductor stocks were among the strongest performers with the SOOX +3%, while memory names rallied around 7% ahead of Samsung’s preliminary earnings release overnight. Alongside Technology, Communication Services, and Consumer Discretionary outperformed, while the traditional defensive sectors of Health Care, Consumer Staples and Real Estate lagged in a reversal of recent moves. Chip stocks like rebounded as Broadcom outperformed rising more than 5% during the day after extending its partnership with Apple. Microsoft fell 0.9% as it said it was cutting 2.1% of its workforce, roughly 4.800 jobs. Q2 earnings season picks up the pace a little with consumer stocks PepsiCo and Delta Airlines reporting Thursday and Friday this week, ahead of major financials next week. SpaceX closed modestly lower as Elon Musk’s rocket and AI giant gets ready to join the Nasdaq 100. Its fast track into the tech-heavy index may have lifted international demand for US tech investment exposure.

Asian Stocks: Futures are green. APAC stocks reversed early gains ahead of a big week with Samsung Q2 earnings and SK Hynix’s US listing. The ASX 200 saw strength in Energy and Health offset by weakness in Minnig and Consumer Staples. The Nikkei 225 was soft as it pulled back from recent record highs. The Shanghai Comp and the Hang Seng were mixed with the latter beating the former. Alibaba found some comfort after a US federal judge ordered the Pentagon to give it a reprieve from a lobbying ban tied to the Pentagon’s curbs on Chinese companies.

Gold rose for a third straight day as bugs tried to make a big base above and around $4,00. The 50-day SMA has moved below the 200-day which is a bearish death cross, but the timing can sometimes be variable.

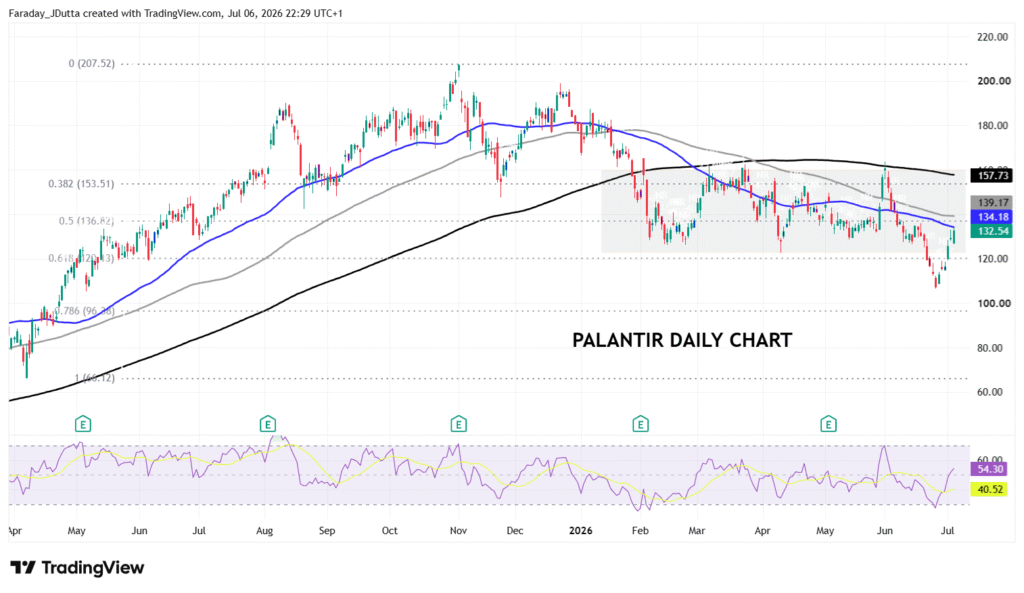

Chart of the Day – Palantir rebounds back to 50-day SMA

PLTR had been trading in a range between roughly $123 and $160, with the upside capped on three main occasions this year in early and late March and June, by the 200-day SMA, now at $157.73. Prices dipped lower in the latter part of June to a near 14-month low at $108.47. But the software company rebounded sharply last week and enjoyed its six straight day of gains. The 50-day SMA sits just above at $134.18 and the midpoint of the April 2025 low to November 2025 high at $136.82. Stronger competitive positioning as enterprises seek flexibility while depl0ying generative AI is helping support stocks prices more broadly.