Tech trounced as semis sink; Dollar dominant

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Iran and Oman say they’ll work on pact for Hormuz transit costs

* Trump keeps claiming Iran made concessions, Iran keeps denying them

* Dollar rises to 13-month high on Fed hike bets, safe haven bid

* S&P 500 falls on global chip rout with Nasdaq off more than 3%

FX: USD pushed up to fresh cycle highs towards 101.50. Risk-off sentiment is helping while expectations of US divergence on growth, inflation and monetary policy are underpinning the current strong USD momentum, for now. Markets can also point to comments from the Fed’s Goolsbee on Monday, (“inflation is going the “wrong way”) to support to the hawkish Fed narrative which hit markets after last week’s FOMC meeting. That said, numerous reviews have been set up by new Chair Warsh, which may take some time to complete and act on. The DXY is now overbought on some measures.

EUR broke down through the mid-March 2026 low at 1.1410. Risk aversion is helping the greenback while eurozone PMI figures were largely in line. Some ECB comments were hawkish, but they went against President Lagarde’s on Monday. These were deemed mildly dovish as she said there is no need to step up the monetary response to the war, as she has confidence that inflation is headed back to the target in the medium term. A Q3 rate hike remains largely priced in.

GBP outperformed most of its peers even as PMIs were modestly softer in both manufacturing and services, which printed sub-50 contraction. Focus was on the domestic political scene with PM-elect Burnham set to deliver a speech next week where he will outline his economic plan. Fiscal risk remains a core concern for markets as participants look specifically to the choice of Chancellor. Burnham is a left-leaning candidate, and markets may struggle to remain confident in the UK’s fiscal outlook without a clear re-commitment to the self-imposed fiscal rules championed by current Chancellor Reeves.

JPY printed an inside day doji, as the yen outperformed against the dollar which was strong against the other majors. Overnight, Japanese Finance Minister Katayama confirmed she spoke with U S Treasury Secretary Bessent on Monday. APAC trade saw stronger flash PMI data with Japan’s manufacturing and services improving on the month. The long-term USD/JPY top from July 2024 sits at 161.95.

US stocks: The S&P 500 lost 1.44% to close at 7,365, the Nasdaq closed down 3.29% at 29,347 and the Dow Jones settled lower by 0.09% at 51,672. Sector performance was mixed. Technology fell by over 3%, while Industrials and Materials also lagged. In contrast, traditional defensive sectors outperformed, with Consumer Staples, Real Estate, Health Care and Utilities all finishing in positive territory. That meant the Nasdaq was the clear laggard while the Dow Jones outperformed, reflecting continued pressure on AI-related names.

Gains in IBM buoyed the Dow after receiving an upgrade at JPM and positive commentary from US President Trump on quantum computing and IBM stock. The primary driver of the weakness was another round of selling in semiconductor and memory stocks, after a sharp decline in South Korean equities overnight, where both SK Hynix and Samsung came under heavy pressure. While there was no obvious headline catalyst, the move may reflect profit-taking and positioning adjustments following the sector’s powerful rally earlier this year, particularly after last week’s hawkish FOMC decision pushed Treasury yields higher.

A key driver of the weakness in the Nasdaq and the S&P 500 was pressure on Nvidia (-3.7%), as its market cap fell below $5 trillion as semiconductors plunged across the board. Micron dropped over 13% ahead of its earnings after the close. SpaceX steadied and added 1% after its own plunge on Monday as it revealed plans around AI infrastructure spending.

Asian Stocks: Futures are mixed. APAC stocks traded muted with choppy price action again after mixed Wall Street performance. The ASX 200 traded little changed as financials and defensive strength were offset by tech and commodity weakness. The Nikkei 225 was close to another fresh record high before changing course sharply. The Hang Seng and Shanghai Comp were subdued with the former undone by mining losses and tech rotation.

Gold fell for a fourth straight day though off the prior late March spike low at $4,098. The stronger dollar and higher real yields are hurting the non-yielding asset. Goldman Sachs cut its year-end target to $4,900 from $5,200. They say every 50bps worth of rate cuts adds roughly $120 support to bullion.

Day Ahead – Australia CPI

Australia inflation is expected to cool in May, with consensus forecasting a 0.3% m/m decline and annual inflation of 4.3% y/y, driven by lower fuel prices. The RBA’s preferred inflation measure, the trimmed mean, is forecast to rise 0.4% m/m and 3.6% y/y, although uncertainty around the strength and speed of price adjustments remains a key downside risk. Surveys point to businesses absorbing cost increases, while demand conditions made it difficult for firms to pass through higher input costs. One business survey also indicated that price pressures peaked in April. Overall, a trimmed mean in line with expectations will keep the RBA on hold at its next meeting in August, which sees roughly 6bps of tightening priced.

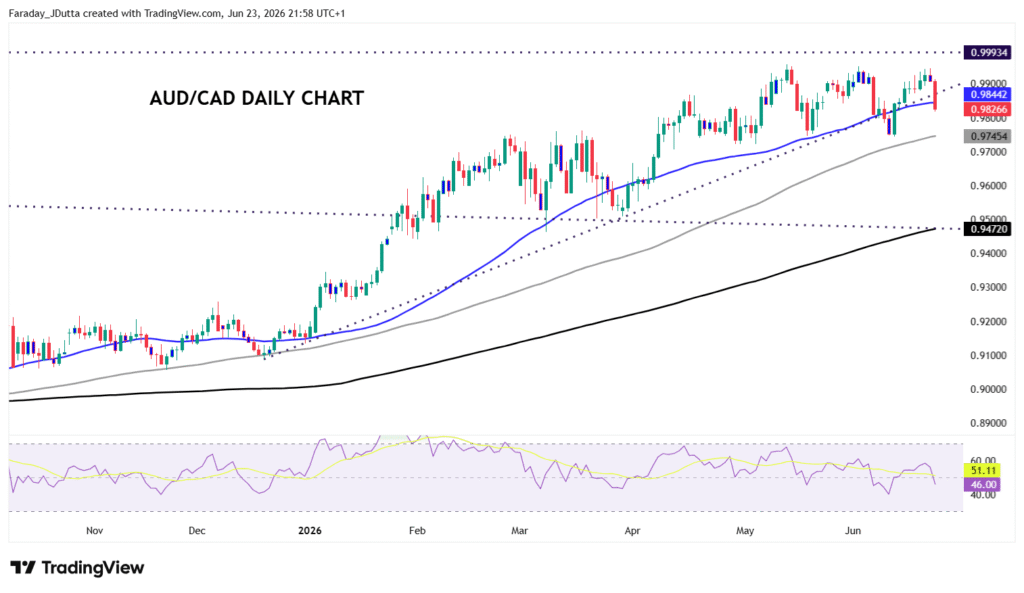

Chart of the Day – AUD/CAD pulls back after hitting resistance

AUDCAD bumped up again into a resistance zone around 99.50 and sold off quite sharply on Tuesday. Bullish momentum had recently picked up with the aussie holding major gains through recent highs around 0.98 and before that 0.95 which was a very long-term resistance line. Trend momentum signals pulled back across multiple timeframe signals, and we’ve broken this year’s up trendline from December. Bulls will want to hold the 50-day SMA at 0.9844 to attack again the 0.9850 zone and top from February 2021 at 0.9993. A conclusive push above par would clear the way for additional AUD gains towards 1.03/1.05.