More record stock highs despite oil gains

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* President Trump says he may go to Islamabad if Iran deal reached

* Israel and Lebanon agree to 10-day ceasefire

* S&P 500 and Nasdaq post fresh record highs on positive earnings

* Crude oil prices rise due to continued Strait of Hormuz closure

FX: USD found a bid, which is unsurprising as we said recently after eight losing days in a row. Prices have found support at the midpoint of this year’s low and high at 98.09. Crude oil prices moved higher as many question marks still linger over an Iran-US ceasefire, with some reports it could take six months. The Fed’s Beige Book showed economic activity flat to modestly expanding, with the K-shaped dynamic in full swing. That means lower-income households were feeling the strain, while higher-income spending remained resilient. The labour market seemed to be holding up well, which all points to a Fed on hold, with eyes on next week’s confirmation hearing of new Fed Chair Warsh.

EUR sold off mildly after a strong win streak and as the major rose close to the major fib level (61.8%) of this year’s know to high move at 1.1826. The March ECB minutes showed that the bank is wary of a premature rate hike due to fears of a new energy-driven surge in the region’s inflation. Officials said there was a lack of sufficient evidence to conclude that the Iran war would durably raise inflation in the bloc. More officials have this week also said the ECB is in no rush to alter rates, and this includes well-known hawk Schnabel. Markets now price in little chance of a hike for the April 30 meeting while June is currently priced at 21bps, down from 25bps over the past week or so.

GBP was modestly lower which is a healthy pause for breath after several days of gains. GDP came in better than expected but seasonals and the fact it is backward looking data saw markets look through the figures. Governor Bailey was on wires and pushed back on policy tightening. Otherwise, sentiment is still the major driver while rates markets continue to fade hike expectations with just less than a coin toss chance of a June move. Bullish momentum in cable has eased with initial resistance in the upper 1.35 area.

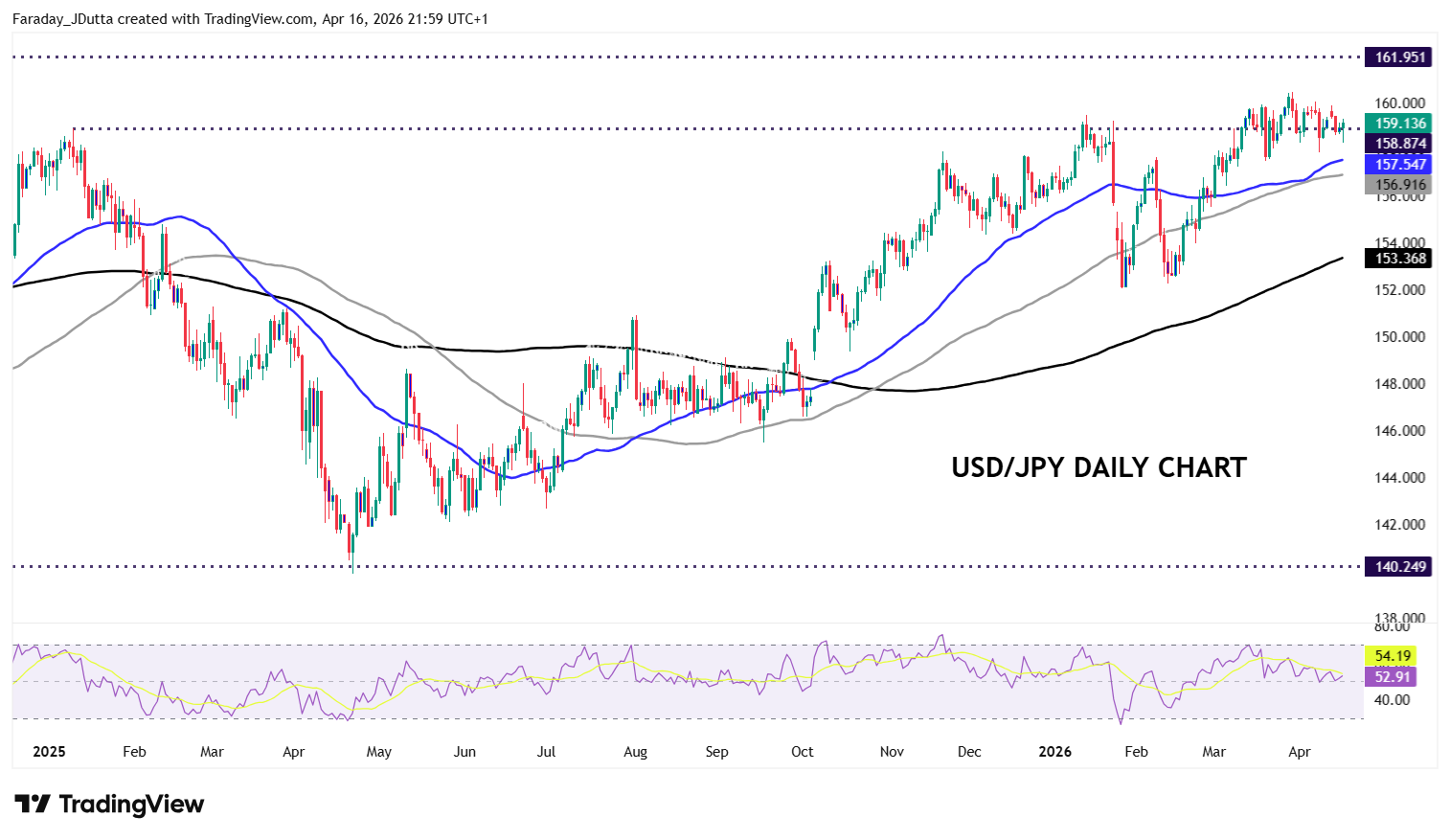

JPY againunderperformed as the major continued to trade around a prior cycle high at 158.87. Finance Minister Katayama and US Treasury Secretary Bessent are said to have had close discussions on Wednesday, and are prepared for ‘bold’ action, essentially a nod to possible intervention. See below for more.

US stocks: The S&P 500 added 0.26% to close at 7,041, the Nasdaq was 0.49% higher at 26,333 and the Dow Jones settled up by 0.24% at 48,579. Most sectors ended higher, led by Energy, Real Estate and Technology, while Healthcare, Industrials and Consumer Discretionary lagged. TSMC, the world’s biggest chipmaker and Asia’s biggest company, beat earnings estimates and raised its full year capex on booming chip demand. But the stock closed lower as the Korean giant warned that increasing component costs, including for memory chips, could impact the price sensitive consumer market. Charles Schwab slid 7% as its results disappointed amid cash management concerns. Netflix tumbled after the close (-8%) as the giant streamer missed EPS consensus by 8% and announced that co-founder Reed Hastings will step down after 29 years.

Asian stocks: Futures are mixed. APAC stocks gained following the strong record move Stateside. The ASX 200 gave back gains as energy and materials losses trumped tech outperformance. Broadly in line jobs data kept hawkish RBA pricing steady. The Nikkei 225 hit a fresh record top above 59,500 as tech stocks boosted the tech-heavy index. The Hang Seng and Shanghai Composite were higher after the mixed Chinese GDP and activity data. Q1 growth missed expectations, but the annual print topped forecasts and printed at the high-end of the official 2026 target. Industrial production data for March was better-than-expected but retail sales disappointed.

Gold was relatively quiet as the dollar and yields pushed higher in modest moves. Higher real rates, a firmer greenback and profit-taking could weigh on near-term price action, though recent pullbacks suggest underlying demand remains resilient.

Day Ahead Thoughts

We note that over the last week, some major investment banks have moved their S&P 500 year-end forecast, both lower and higher. The current median year-end 2026 projection sits around 7,700, so an implied upside of roughly 10%. There is much chatter now on trading desks about the current stock rally being rather unloved.

There was record hedging and selling on the way down and dealers are now covering shorts with the biggest forced buying of positions in the current cycle. Higher stock prices have then triggered automatic rebalancing over sentiment-driven buying. Allied to this, the recent Bank of America fund manager survey showed global investor sentiment reaching its most bearish level since June 2025, based on cash levels, equity allocation, and global growth expectations. All in, markets are currently witnessing both sentiment and positioning rebalancing.

Chart of the Day – USD/JPY consolidating in intervention territory

As detailed above, US and Japanese finance officials have been meeting in Washington with suggestions of closer co-operation and so potential intervention. But barring a big drop in energy prices from here which appears unlikely at present, or much lower US interest rates, this is verbal intervention to the max and an exercise in containing USD/JPY upside. The flips side to this is the current 20% chance of a Bank of Japan rate hike on 28 April that does appear to have room to increase. If that happens, it could help cement the top of the USD/JPY range at 160. But the conditions for a sustained drop in USD/JPY look tough for now. The 2025 high is 158.87 and the recent long-term top at 160.46, with the 50-day SMA at 157.54 and the 100-day below at 156.91.