Historic day in oil as Trump comments calm markets

Jamie Dutta >

Market Analyst

Jamie Dutta >

Market Analyst

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* President Trump says the war could be over soon and is “very complete”

* Oil moves lower from spike highs as G7, Trump seek to calm markets

* Wall Street ends higher as Iran war resolution offsets inflation fears

* Dollar whipsawed on hopes of an end to Middle East conflict

FX: USD gave back nearly all of its gains as oil prices fell through the day but very sharply after Trump’s comments very late in the US session. He said, “the war is complete, pretty much” and the US is “very far” ahead of his 4 to 5 week time frame. Safe haven demand was initially evident with narrowing interest‑rate differentials versus key peers, as central banks excluding the Fed may have responded more forcefully to increasing price pressures with rate hikes. De-escalation should see the buck give back some of its haven gains The index found resistance again around last week’s spike high at 99.68. Long-term support sits at 98.70 with the 100-day SMA at 98.56.

EUR finished on its highs as oil prices reversed their spike overnight Asian session peaks. The single currency has been hit due to the negative energy-driven terms of trade shock, with the block a net importer of energy. IEA relief supply helped through the day, while rate differentials also support the euro. That said, the 45bps of ECB rate hikes priced in for this year has been reined in and markets will continue to walk some of that back.

GBP has been mid-pack to outperforming slightly among its peers over the past week. Cable consolidated some more below its 100-day SMA at 1.3394 through most of the day, before Trump’s comments pushed it up to the 200-day SMA at 1.3440. Money markets had shifted rates in Asian hours to just a 50% chance of one 25bps cut this year versus two quarter points reductions last week. The midpoint of the November to January low to high move sits at 1.3439 with the 50-day SMA at 1.3525.

JPY strengthened through the day as the major came off its high at 158.89. We were nearing intervention or at least ‘rate check’ territory but the major closed on its lows below 158. Focus may turn to next week’s BoJ meeting and comments about any more policy tightening.

US stocks: The S&P 500 added 0.84% to close at 6,797, the Nasdaq was 1.32% higher at 24,967 and the Dow Jones settled higher by 0.5% at 47,741. Tech led the gainers with Communication Services and Healthcare also big winners, while just Energy and Financials were in the red. The semiconductor index rebounded with Sandisk up jumping 11.6%, Broadcom up 4.6% and Nvidia adding 2.7%. It will be interesting to see if the recent cyclical outperformance in the US and European underperformance continues if conflict concerns ease. The HALO (heavy asset, low obsolescence) theme that had been key through February has unwound somewhat even amid rising geopolitical tensions.

Asian stocks: Futures are green. APAC stocks fell sharply as oil prices spiked higher on little sign of any de-escalation amid more producers cutting output. The ASX 200 slumped with heavy losses across all sectors apart from energy. The Nikkei 225 plunged over 5% as manufacturers and exporters suffered from the rising energy costs and shipping disruption. The Hang Seng and Shanghai Comp conformed to the broad risk-off mood with sources tempering expectations for a breakthrough in the upcoming Trump/Xi summit. Downside in the mainland was somewhat cushioned after 37-month high Chinese inflation data.

Gold was mixed again as the rising dollar didn’t help bugs through most of the day. Treasury yields eventually fell on the day which helped bullion close near its highs.

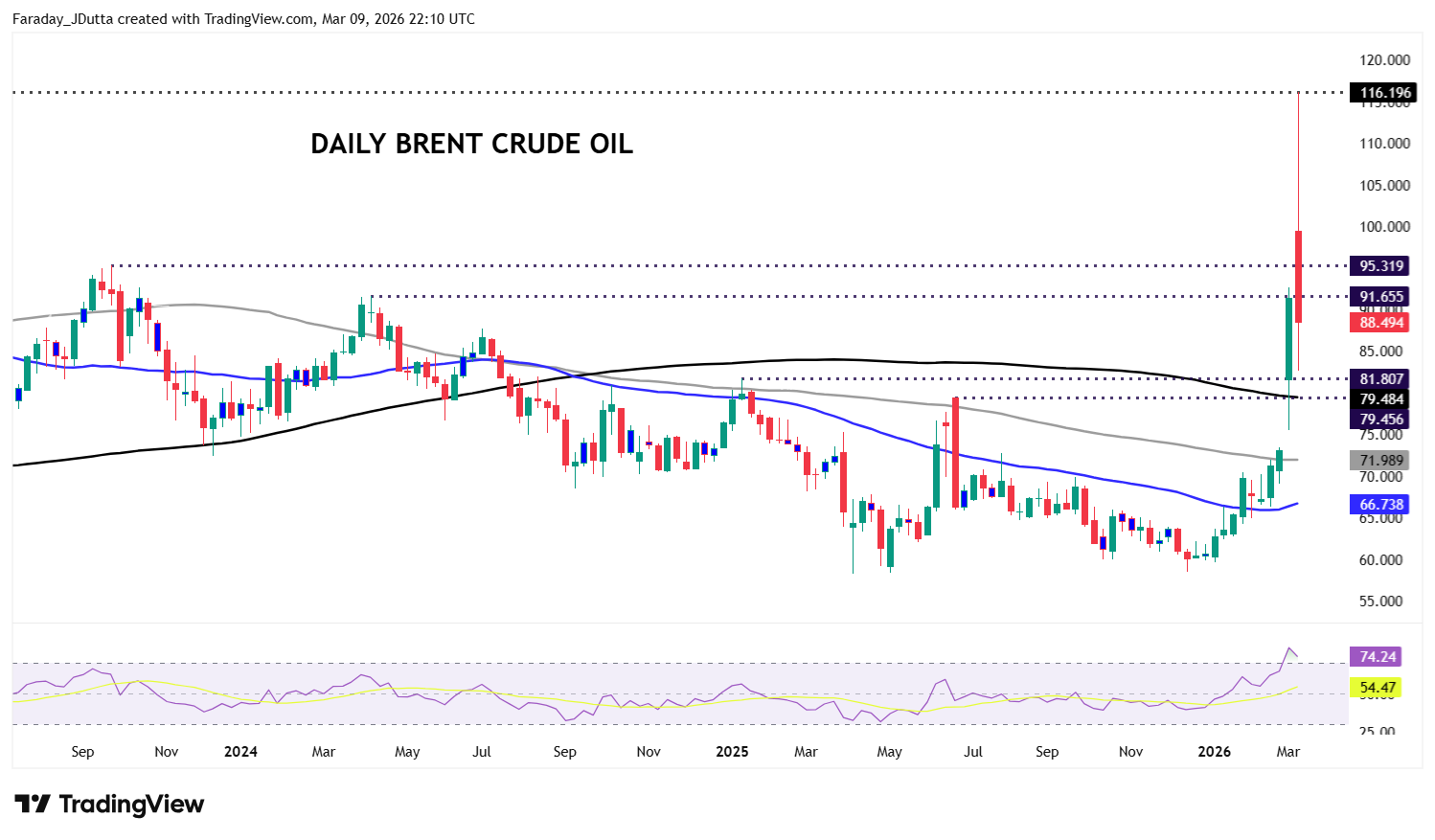

Chart of the Day – Crude’s historic day

Brent had an astonishing near 30% intraday move as headline havoc hit oil markets in full effect. It soared through the hugely psychological $100 marker and briefly traded above $116 in thin Asian hours. The war seemed like it was getting worse, not better. Producers in Iraq, Kuwait and the UAE started to shut wells because they can’t move crude out, which meant a big hit to supply in a very short time. Even if tankers start moving through the Strait of Hormuz again, you can’t instantly restart this production.

Through the day, major governments and agencies endeavoured to step in with a big, coordinated release of emergency oil reserves. Pressure for that grew the longer crude stayed above 100. Interestingly, recent positioning showed many speculators actually cutting exposure in Brent. That’s not because the story is bearish, but because the news flow has been so unpredictable. The mix of tight supply and nervous positioning created big two‑way volatility. The Russia-Ukraine high was just above $130, with other notable tops at $99.05, $95.31 and $91.65. The January 2025 sits at $81.80 with the 200-day SMA at $79.48.