Geopolitical headline swings cause choppy markets

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* ‘Intense mediation’ underway with Pakistani officials in Iran

* President Trump vows US will retrieve Iran uranium

* S&P 500 wavers in volatile trading for oil, NVDA drops after earnings

* Walmart reports solid results but sees some consumers struggling

FX: USD was little changed after making fresh cycle highs just before the US open. The DXY remains above the 50-day SMA at 99.20. According to Reuters and Politico, the two key sticking points between the US and Iran remain Iran’s nuclear programme and reopening the Strait of Hormuz. Reuters also reported that no deal has yet been reached, although negotiations have narrowed the gaps between both sides. Treasury yields slid for a second day as Brent crude printed a doji on the 50-day SMA.

EUR dipped but moved off its lows as PMIs came in softer than forecast and signalled rising recession risks in the region if the Middle East conflict continues. French data saw the biggest contraction since late 2020 while the region’s composite and services fell further into contraction below 50. The composite was the lowest print since 2023. Sentiment remains the biggest driver though, as market oscillate on the headlines around war and peace.

GBP outperformed most of its peers again, as cable continued to trade around the 50 and 200-day SMAs at 1.3427/21. It printed an inside day and doji denoting uncertainty. The PMIs were mixed with manufacturing better, but services unexpectedly fell into contractionary territory. Wes Streeting, a potential challenger to PM Starmer said he wouldn’t challenge Andy Burnham, if he wins the by-election to become an MP.

JPY continued to consolidate around the 2025 top and 50-day SMA around 158.87/76. BoJ officials were on the wires again with a second non-dissenting member indicating a willingness to tighten policy. That means the prior meeting’s 6-3 vote split could be vulnerable. Money markets currently price in a near 80% chance of a rate hike in June with 48bps for 2026.

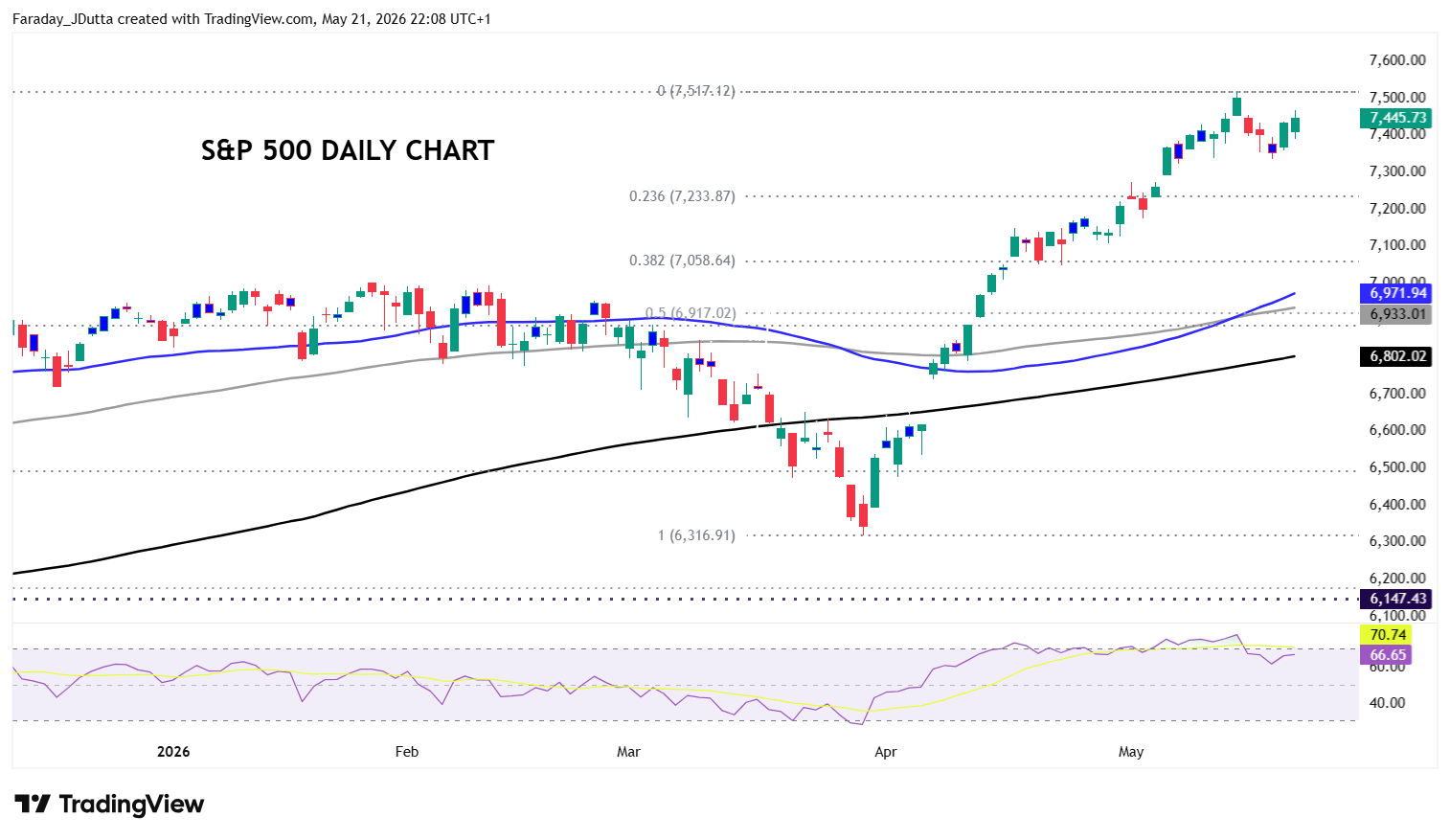

US stocks: The S&P 500 added 0.17% to close at 7,446, the Nasdaq closed up 0.20% at 29,357 and the Dow Jones settled higher by 0.55% at 50,291. Most sectors were positive with Utilities, Consumer Discretionary and Materials leading the gainers, and Consumer Staples and Energy down more than 1%. Nvidia closed lower by 1.8% as profit taking and sky-high expectations was the shares lag even as the giant chipmaker released blockbuster numbers and raised guidance. Walmart fell 7.3% after it beat on the top line but issued a worse than expected outlook as high gas prices hit shoppers. The mega retailer said high tax returns may have muted some of the impact of elevated gas prices on shoppers, signalling consumer pressures could rise in the current quarter. Memory and chipmakers surged with Sandisk up 10.8% and Nebius surging 14.7%. The former saw Citi lift its price target to $2,025 on stronger storage demand and tighter supply conditions. The NVDA outlook boosted Nebius and NBIS partnered with Bloom Energy to speed up AI power expansion.

Asian Stocks: Futures are mixed. APAC stocks were mostly bid after the Wall street rally on increased Middle East peace optimism and falling crude oil prices. The ASX 200 saw gains led by real estate, mining and materials while shrugging off weak jobs and PMI data. The Nikkei 225 surged higher on strong tech buying and as Softbank jumped around 20% after the blockbuster Nvidia earnings. The drop in energy prices also helped. The Shanghai Composite and Hang Seng lagged their regional peers amid weakness in energy and automaker stocks.

Gold continues to consolidate just above the minor Fib level of this year’s high-to low move at $4,452. The mixed dollar hindered bugs on Thursday as optimism around a peace deal was also mixed. The 200-day SMA is $4,346.

Day Ahead – UK Retail Sales

Retail sales activity in the UK is likely to fall due to the timing of Easter and weaker consumer confidence, with food and big-ticket items hit. The headline print is forecast at -0.3% m/m after the 0.2% rise in March. Frontloading of fuel sales may offset this as motorists filled up heading into the Middle East conflict while the fourth sunniest April since 1910 might have hastened purchases of summer clothes.

This data comes after the usual mid-month UK data dump of jobs figures and inflation numbers, which has generally come in softer than expected. This questions the need for aggressive rate hikes with many economists not especially agreeing with the 70bps+ of tightening that had been priced in prior to the data. A July rate hike is now less than a 50:50 bet, with only now a very small chance (11%) of a move next month.

Chart of the Day – S&P 500’s bullish pullback

Nvidia’s earnings have effectively brought an end to the reporting season. With 93% companies having reported, the key point is that it has been an extremely strong earnings season. We’ve had 10% revenue growth and 20% earnings growth with earnings beating by 10%. Similar to recent years, the tech sector has delivered the most impressive numbers, with 30% top-line growth and 50% bottom-line growth. In other words, the reporting season has been far stronger than analysts expected going in, and we have seen one of the strongest earnings-revision cycles through Q1 reporting in many years. For the broader market, the wall of worry around the huge scale of AI investment ($750+ billion in 2026), wars in the Middle East and Ukraine and fiscal concerns among others has been ‘trumped’ (pardon the pun) by both revenue and earnings growth running much faster than expectations. The S&P 500’s rebound from the late March low was close to 20% before the healthy recent pullback. The record high sits at 7,517.