Dollar rebound restarts while stock slide continues

Jamie Dutta >

Market Analyst

Jamie Dutta >

Market Analyst

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Stronger dollar pulls down gold with Fed rate path in question

* Wall Street eases on Powell remarks ahead of PCE data

* Tesla jumps on positive broker analyst reports, Q3 deliveries

* Treasury yields inch higher driven by busy bond supply

FX: USD jumped as its rebound from multi-year lows gathered mild bullish momentum with the daily RSI moving above 50. The 50-day SMA on the Dollar Index sits at 98.03. Markets are still digesting Powell’s comments about the tricky balance between upside inflation risks and downside labour market concerns. It appears he is still focused on this, while the consensus at least according to the median dot plot for this year, side with the softer jobs data and two more 25bps rate cuts this year. Markets currently give that around a 75% chance, with above 90% of the first one in October.

EUR slid as German IFO business survey data disappointed. Business climate, current conditions, and expectations all fell. It appears that eurozone growth momentum remains weak despite hopes that government spending would boost activity. Initial support sits at a minor Fib level of the August bull move at 1.1717.

GBP marginally outperformed against the dollar but still settled below its 50-day SMA at 1.3467. There was little UK news though BoE Governor Bailey said there is still further room to cut rates, and the extent depends on the path of inflation. MPC member Greene was also on the wires, stating that the bank should take a cautious approach to rate cuts going forward.

JPY underperformed as the major moved above the 200-day SMA at 148.50 with a strong close. Bullish momentum has picked up after the false breakdown last week. Buyers will target 149.37 and 150.91. Comments from LDP leadership candidate front-runner Takaichi, a monetary and fiscal dove, who said the BoJ should be left to set monetary policy, didn’t impact much.

AUD outperformed its major peers versus the dollar but went red through the day. Strength came from firmer CPI data which saw the annual rate climb two-tenths to 3%, which is the top end of the RBA’s range. CAD softened as the major got close to the swing high from late August at 1.3924. Interest rate differentials continue to widen out and keep the defensive tone around the loonie.

US stocks: The S&P 500 lost 0.28% to close at 6,638. The Nasdaq settled lower by 0.31% to settle at 24,504. The Dow Jones finished at 46,121, down 0.37%. Only four sectors were positive with Energy again the clear leader as crude rose for a second straight day. Materials led the laggards, with Real Estate and Communication Services making up the bottom three worst performing sectors. Micron dropped 2.8% despite posting stronger than expected earnings while Nvidia slipped 0.82% as investors had concerns about energy demand and competition. In contrast, Alibaba’s pledge to boost AI spending lifted its stock over 8% while Tesla jumped 3.98% after a wave of positive Wall Street analyst notes and upbeat forecasts for Q3 vehicle deliveries.

Asian stocks: Futures are mixed. Stocks traded mixed again as soft sentiment Stateside impacted, as well as the Super Typhoon. The ASX 200 slid on gold mining profit taking, with tech also lower. The Nikkei 225 moved lower after its holiday break though losses were cushioned by the Nvidia/OpenAI rally. The Hang Seng and Shanghai Comp eventually went green with Alibaba the standout performer. It surged after releasing its largest LLM whilst also announcing plans to ramp up spending on AI infrastructure to better compete with US rivals.

Gold paused for breath after its stunning rally this month and year. We wrote that a correction was due yesterday, with prices heavily overbought. Bets on Fed rate cuts, so lower funding costs have been reined in modestly after Chair Powell’s continued cautious stance.

Day Ahead – SNB Meeting

The Swiss National Bank (SNB) is likely to keep rates unchanged at 0%. This comes after the bank delivered a quarter-point cut in its June meeting, which ended the period of positive rates. Recent inflation data printed in line with expectations. Stronger evidence is needed of cooler prices; with many economists reckoning we are now at the terminal rate.

In fact, the bar to dipping into negative rates territory is high, according to Chairman Schlegel, even though he has said rate setters won’t hesitate to go there, with the SNB aware of their undesired side effects for savers and pension funds. The market prices in around 12bps of easing in the next 12 months.

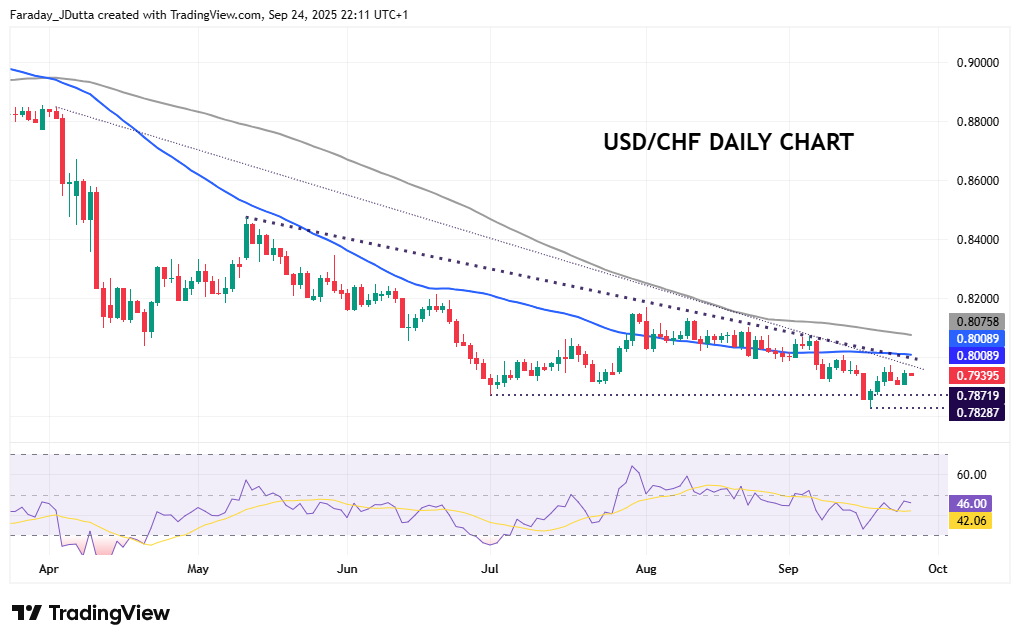

Chart of the Day – USD/CHF long-term downtrend still in play

The SNB is well known to be sensitive to CHF rates and the headache caused by a strong Swiss franc in 2025 will not be lost on policymakers. The swissie has rallied by over 14% against the dollar year-to-date and is set for its largest annual gain since 2002. For Swiss exporters, such as Nestle, Novartis or Richemont, currency strength adds to hefty U.S. tariffs. After printing multi-year lows going back to 2011 at 0.7828 after last week’s FOMC meeting, prices have staged a mild recovery. That has moved above the prior cycle low at 0.7871 which printed at the start of July. A medium term downward trendline sits near the 50-day SMA at 0.759, reinforcing this initial resistance zone. The 100-day SMA sits above at 0.8011.