Weekly Outlook | Limited Data With the Focus on Geopolitical Tensions

Important events this week:

Last week, stock markets resumed upside momentum again with in particular the Nasdaq index trading close to previous highs. The positive sentiment might resume pace as the issues in regards to regional banks in the United States have clamed down. Furthermore, statements from Jerome Powell, the chairman of the Federal Reserve in the United States, pointed out that he is prepared to continue cutting rates further. Fresh liquidity is hence expected and will support stocks rising.

The various consumer price indices as well as purchasing manager indices might move markets as well. Yet, the big news in regards to US data like the absence of the Nonfarm payrolls report due to the ongoing shutdown in the United States is still due at some point and might offer more clarity for traders when they will be released.

On another note, also the meeting between US President Trump and Russian President Putin might offer clarity for market participants. Any chance, that the Ukraine will come closer to peace might help European stocks moving higher.

US Consumer price index: The consumer prices index from the US might move markets. It is expected to come out at 0.4% month over month yet being delayed due to the shutdown. The rate of inflation remains stubborn and hence the data will likely be eyed with caution. A falling rate might support the US Central Bank to cut rates further, which would likely cause the Dollar to weaken.

The strong trend in Gold has not shown any signs of a correction and instead keeps continuing to the upside. A weaker Dollar might still help the shining metal. Vice versa a stronger reading could cause the market to correct pushing God back towards the USD 4,000 level, where the next support zone can be found. The release of the CPI data will take place on Friday, 24th October at 14:30 CET.

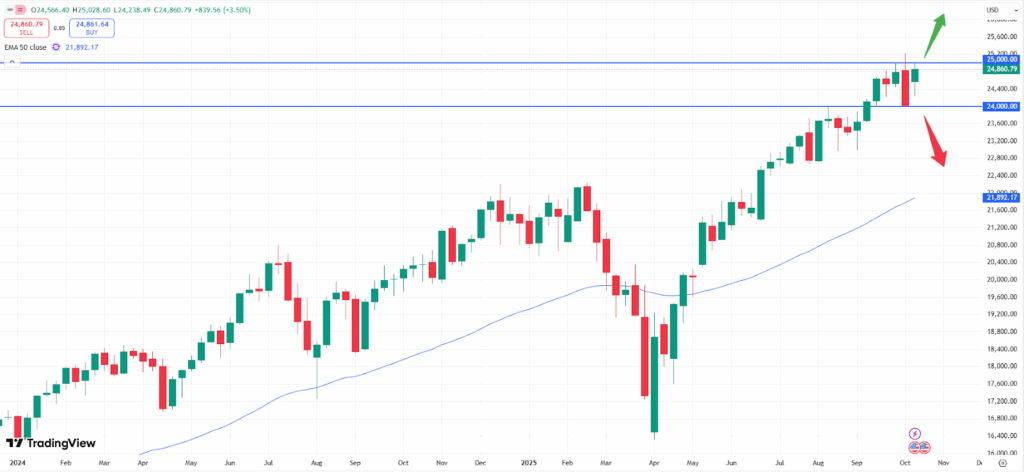

US PMI data: Both purchasing manager indices, the manufacturing as well as the services pmi data might cause the Nasdaq to move as well. A better-than-expected reading might show positive signs for the development of the economy, while a weaker figure might cause the market to weaken.

Currently, the Nasdaq index seems capped between important zones. While the upside beyond the 25,000 level still seems a strong resistance, a lower reading below the 24,000 mark might offer a further correction. Markets have been resilient in recent weeks and a correction in the market will be healthy for the current bullish trend. If the market will break the important support zone the losses might intensify towards the 22,000 level, before buyers will step in. The data will be released on Friday, 24th October at 15:45 CET.