Think the US dollar always climbs higher? Well, 2025 is proving otherwise. After years of flexing its “King Dollar” muscles, the greenback has stumbled. It recorded its worst first six months of a year since the early 1970s.

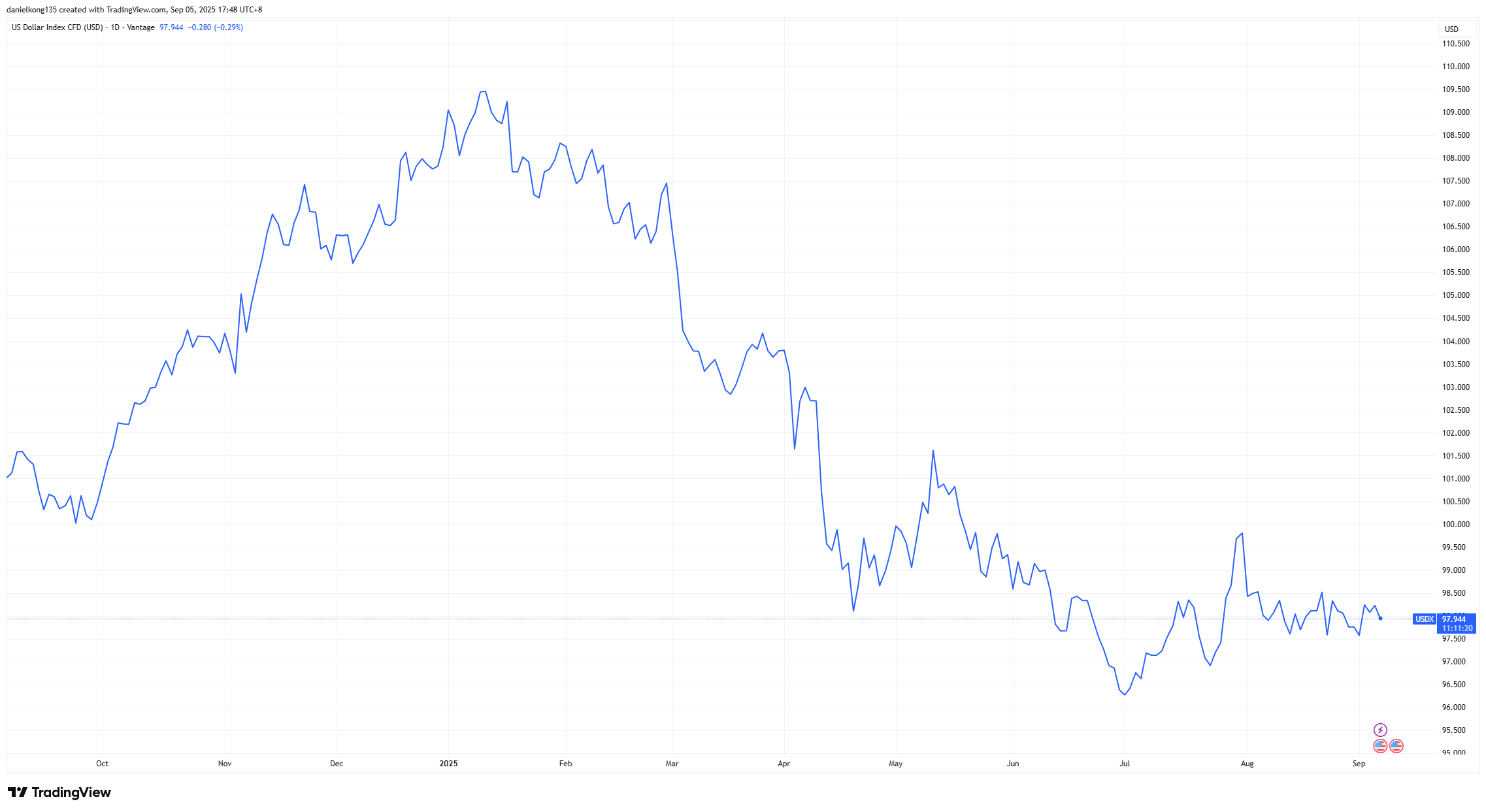

As of 3 September 2025, the US Dollar Index is hovering near 97.8, down almost 9.6% year-to-date and only slightly above a 52-week low [1].

That is a decisive break from its 110 peak earlier this year. The impact is already visible: commodities are recalibrating, multinational earnings are shifting, and emerging markets are breathing easier.

No, the dollar is not collapsing. But its stumble is changing the rules of the game. For eight decades, the dollar has served as the world’s financial operating system, dominant in trade invoicing, central-bank reserves, and global borrowing costs.

That is why this decline matters. The real question is not whether the greenback has lost its crown (it has not), but whether 2025 marks the start of a new chapter where its grip begins to loosen.

Key Points

- The US dollar has weakened in 2025, driven by shifting Federal Reserve policy, fiscal strains, and rising geopolitical tensions.

- A softer dollar impacts commodities, emerging markets, and corporate earnings, creating ripple effects across global trade and investment.

- While alternatives like the euro, yuan, and digital currencies are gaining traction, the dollar remains the dominant reserve and trade currency for now.

The US Dollar’s Global Role

Before exploring the dollar’s recent weakness, it is important to understand why the currency has long been at the centre of global finance and why its resilience has been underestimated time and again.

Why the Dollar Matters

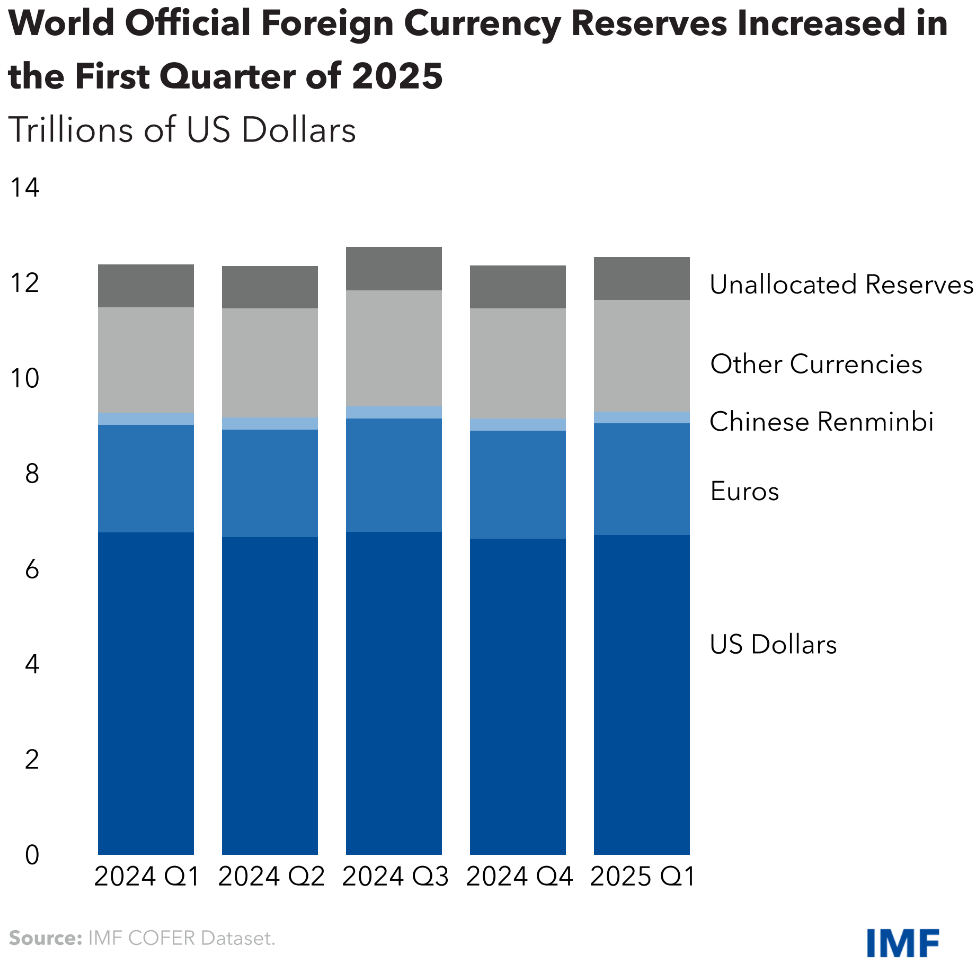

It is difficult to overstate how central the US dollar is to the world’s financial plumbing. Roughly 60% of global foreign-exchange reserves are held in dollars. Most international trade, from crude oil to microchips, is denominated in dollars, regardless of whether the US is involved.

Global debt markets are anchored to the greenback as well, with trillions in bonds and loans benchmarked against US rates. Think of the dollar as the iOS or Android of global finance: most transactions are built to run on it.

That dominance provides the US with structural advantages; lower borrowing costs, deeper liquidity, and the ability to fund deficits in its own currency. For investors, the dollar is not simply part of another currency pair on a screen; it is the tide that influences nearly every asset class.

Historic Resilience

This is not the first time skeptics have bet against the dollar. In the 1980s, rising US deficits prompted predictions of collapse. During the 2008 Global Financial Crisis (GFC), despite being the epicentre of turmoil, the US still attracted safe-haven flows into Treasuries.

After pandemic-era stimulus and money printing, the dollar surged again in 2022 as the Federal Reserve hiked aggressively. The lesson is clear: the dollar has a track record of defying predictions.

When global uncertainty strikes, investors still reach for the greenback. That is why the 2025 decline feels less like an obituary and more like a plot twist. Alternatives are emerging, but none yet offers the same trust, liquidity, or scale.

What Is Driving the Dollar’s Decline?

With the dollar’s position established, attention turns to the immediate and structural factors that have pushed the currency lower in 2025. These forces span policy, economics, and geopolitics.

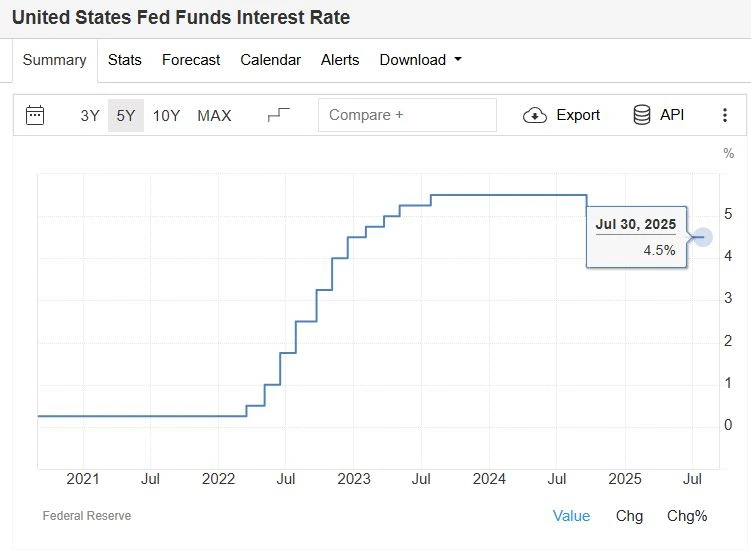

1. Interest Rate Expectations

The most immediate driver of 2025’s dollar weakness is shifting Federal Reserve (Fed) policy on interest rates.

After two years of aggressive tightening, officials are signaling cuts as inflation eases and the labour market cools. Markets are focused on the September FOMC meeting, where a first cut looks increasingly likely.

Lower expected yields shrink the gap between US rates and those abroad. Because currency flows are highly sensitive to interest rate differentials, the dollar loses some of its premium. In simple terms: the carry trade is losing fuel.

2. Fiscal and Economic Pressures

The US fiscal backdrop is another concern. Washington is projected to run a deficit of about $1.7 trillion in FY2025, one of the largest peacetime shortfalls in history [2].

Combined with a rising debt load and slower growth outlook compared to 2023–2024, confidence in US sustainability is weakening. Currencies trade as much on trust as on fundamentals, and cracks in fiscal credibility erode confidence in the greenback at the margins.

3. Geopolitical Shifts

Then there’s the slow burn of geopolitics, and in 2025, the fire has been fanned by President Trump’s sweeping tariff blitz. Call it de-risking, friend-shoring, or re-wiring: the world’s trade and capital flows are shifting in response.

Tariffs covering imports from the EU, Canada, India, and more have rattled supply chains and prompted trading partners to explore non-dollar settlement options and regional currency use. Central banks are quietly diversifying their reserves.

That doesn’t dethrone the dollar, but it nudges the system toward diversification. Every tariff headline or diplomatic flare-up chips away at the greenback’s once-unquestioned dominance.

Layered onto that is a frontal assault on the Fed’s independence. In August 2025, President Trump attempted to fire Federal Reserve Governor Lisa Cook, an unprecedented move that intensified concerns that monetary policy could be politicised and further damage confidence in the dollar’s credibility.

Global Ripple Effects of a Softer Dollar

A weaker greenback does not only matter for US policy makers. Its decline has ripple effects across commodities, emerging economies, and corporate earnings worldwide.

Commodity Markets

Because commodities are priced in dollars, changes in the greenback historically influence their prices. In 2025, gold reached record levels, reflecting lower real yields and a softer dollar.

Oil has been more complex: a weaker dollar offers support, but growth concerns and supply dynamics cap the upside.

Emerging Markets

For emerging economies, dollar weakness feels like relief. A strong dollar typically tightens financial conditions and weighs on growth. A softer dollar lowers debt-servicing costs on dollar-denominated bonds and improves capital flows.

In 2025, EMs have already shown resilience despite tighter global policy, and a continued soft dollar could offer further breathing room.

Multinational Corporations

For US companies, a weaker dollar is an earnings story. Around 40% of S&P 500 revenues come from abroad. When those profits are converted back into the greenback, they are worth more in dollar terms.

Exporters may experience changes in relative pricing. Together, these factors demonstrate how foreign exchange (FX) swings have historically affected earnings seasons alongside other business developments.

The Shifting Balance of Global Currencies

As the dollar loosens its grip, other currencies and even digital money are stepping forward, each with varying degrees of influence and credibility.

Euro and Yen as Alternatives

When the dollar slips, investors usually pivot toward the euro and yen. The euro benefits from institutional heft and credibility, making it the natural absorber of flows. The yen, while still seen as a safe haven, is hampered by a wide yield gap with the US. That limits its ability to rally significantly.

Neither is poised to dethrone the dollar. At best, they act as understudies, stepping into the spotlight occasionally, but not rewriting the script.

The Rise of the Yuan

No discussion of dollar alternatives is complete without China’s ambitions. Beijing continues to push the yuan’s role in trade settlement, with high-profile deals inked in energy and commodities.

But here’s the reality check: the renminbi still accounts for only about 3% of global payments, and even Chinese companies often default to the dollar in cross-border invoicing.

Progress is happening but it’s at a glacial pace. For now, the yuan is more like a regional player than a global reserve juggernaut. An important currency to watch but nowhere near challenging the hegemony of the dollar.

Could Digital Currencies Play a Role?

And then there’s the wild card: digital money. Central bank digital currencies (CBDCs) have moved past the whiteboard stage. Projects like mBridge, which reached “minimum viable product” status in 2024, are now under the wing of central banks themselves.

The idea isn’t to topple the dollar; it’s to make cross-border payments faster, cheaper, and less reliant on the dollar’s plumbing.

If CBDCs scale, they could chip away at the greenback’s transactional dominance over time. But that’s a medium-term story, not a 2025 headline. For now, they’re more promise than practice.

Implications for Global Markets

These shifts are not just currency stories. They influence how traders and investors interpret risks, allocate capital, and respond to volatility.

Traders’ and Investors’ Reactions

The dollar’s 2025 slide has been unusual. Rather than a mass exodus from US assets, much of the move has been hedging-driven, as investors outside the US adjust their exposure.

Historically, dollar weakness has influenced:

- US multinationals’ reported earnings in dollar terms

- The valuation of non-US equities when converted to dollars

- Commodities and gold prices in dollar terms

In short, dollar moves ripple across asset classes far beyond forex charts.

Risk and Volatility Considerations

But a softer dollar doesn’t mean “easy mode” for investors. Dollar cycles tend to be powerful and lumpy, with US policy shocks echoing globally through what the BIS calls the “global financial cycle.” That means swings in the dollar can amplify risk moves in equities, bonds, and credit.

There is also the commodity-dollar nexus to consider. A cheaper greenback can shift the macro buffers of commodity-importing nations, altering their inflation and growth outlooks. Add in unpredictable elements such as tariffs, Fed pivots, and patchy global growth data, and the ride is rarely smooth.

History shows dollar weakness has historically coincided with periods of heightened volatility. This reinforces the importance of careful risk management when considering exposure to currency movements.

Bottom Line for the Dollar

The US dollar’s stumble in 2025 is a reminder that even the world’s most entrenched anchor can wobble. With Fed cuts looming, ballooning deficits, Trump-era tariffs, and shifting trade alliances, the greenback faces pressure on multiple fronts.

The effects are already visible in commodities, emerging markets, and corporate earnings, while other currencies, and even digital tokens, inch into the conversation.

Yet the dollar still commands the lion’s share of reserves, trade invoicing, and borrowing benchmarks. Its unmatched depth and liquidity continue to anchor the system. The cracks, however, are undeniable: diversification efforts, geopolitical frictions, and fiscal concerns are slowly eroding its aura of inevitability.

For investors, the question is not whether the dollar will vanish. It is whether its dominance is shifting gradually toward a multipolar system.

Is 2025 another chapter in its long history of resilience, or the opening act of structural change? The answer could reshape trade, capital flows, and investing strategies for years to come.

Reference

- “September’s Secret Weapon? The Dollar Index – Yahoo!Finance”. https://uk.finance.yahoo.com/news/septembers-secret-weapon-dollar-index-155409172.html . Accessed 5 Sept 2025.

- “US budget deficit forecast $1 trillion higher over next decade, watchdog says – Reuters”. https://www.reuters.com/business/us-budget-deficit-forecast-1-trillion-higher-over-next-decade-watchdog-says-2025-08-20/ . Accessed 5 Sept 2025.